Investment bonds are often described as a cross between a life insurance policy, a superannuation account and a managed fund. Investors put their money into a managed investment portfolio, which is taxed internally and I beneficiary or beneficiaries may be nominated in the event of the life insurance death during the investment term.

Investment bonds are primarily governed by the Life Insurance Act 1995, APRA Prudential Standards, the Income Tax Assessment Act 1997, the Income Tax Assessment Act 1936, the Income Tax Rates Act 1986 and Corporations Act 2001.

Investment bonds accommodate a wide range of investment needs such as

- Wealth Creation

- Tax Planning

- Kids’ Education

- Funerals

- Income Exemptions

A funeral bond is also an investment bond that has the added benefit where it may help investors qualify for both income and asset test exemptions if they receive a means-tested pension or benefit from Centrelink or the Department of Veterans’ Affairs.

Tax Advantages

Investment bonds give investors flexibility and efficiency in Australia’s complicated tax regime.

- Taxed at a maximum rate of 30%

- Tax paid proceeds if held longer than 10 years

- Tax free benefits paid on death (not applicable for funeral bonds)

- Tax free transfers between parties

- No capital gain or income distributions

- No tax file number required

- No personal capital gains tax on investment switching

Tax on earnings differ from ordinary investments that are taxed against your marginal tax rate. Investment bonds pays the tax on earnings at the current company tax rate of 30%. However, this may be lower than the 30% company tax rate due to tax credits such as imputation credits and foreign tax credits. This makes investment bonds a tax effective investment solution for those with a marginal tax rate higher than 30%.

Once investment bonds meet the 10-year rule requirement (not applicable for funeral bonds), there will be no personal income tax liabilities on investment earnings and investors do not have to declare any income in their annual tax returns when making withdrawals. Making it especially popular to invest in your kid’s high school education.

10 Year Rule

If an investor makes a withdrawal (partial or full) within 10 years of their initial investment date they will generally need to include a portion of the earnings generated by the investment bond as part of their tax assessable earnings for that financial year. The assessable earnings will depend on the period has been invested.

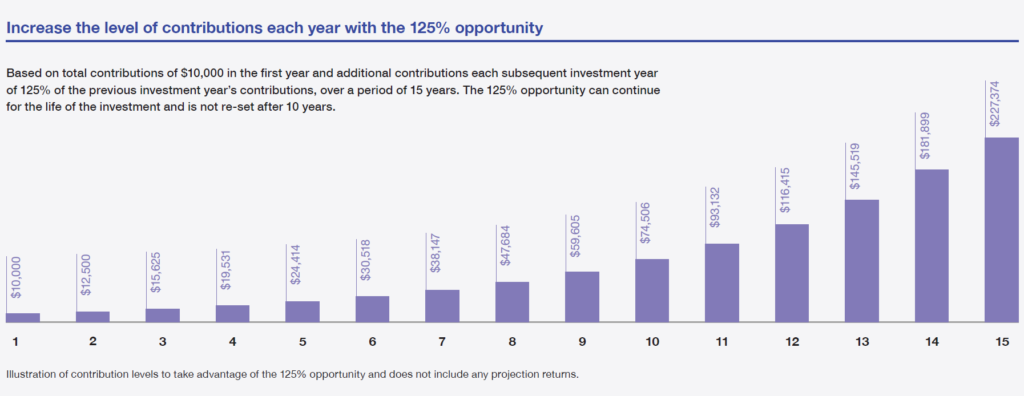

Contributions

Investment bonds are popular because unlike superannuation, where personal contribution amounts are capped and subject to penalty tax rates if exceeded, investment bonds give much greater flexibility on how much can be contributed to an investment.

With an investment bond, there are no limits on the amount you can invest in the first year or how many investment bonds you can own. Each subsequent year, you can contribute up to 125% of the previous year’s contributions without re-setting the 10-year period.

If contributions in the second and subsequent investment years exceed 125% of the previous investment year’s contributions, then the start date of the 10-year rule resets to the year that the excess contributions were made.

Source Generation Life